Real estate and real estate debt have long been characterised by two things: strong investor demand and limited accessibility.

Tokenisation is beginning to address the second element — representing one of the more significant structural shifts in years for an asset class defined by its scale and the barriers to entry that have come with it.

As administrators and fiduciaries, we are seeing growing demand from clients looking to establish and administer tokenised real estate and other private capital structures. This article sets out how these structures work, why Jersey is a natural home for them and what managers and promoters should consider before going to market.

What Is Real-World Asset Tokenisation?

The tokenisation of real-world assets (RWAs) converts ownership rights into digital tokens on a blockchain, placing them on a distributed ledger where each token corresponds to a unit of value in the underlying asset, whether a share of a property or an interest in a debt instrument.

The practical implications are material:

Fractional ownership – large, high-value assets such as commercial property can be divided into smaller tokens, widening access to investors who could not previously participate directly.

Improved liquidity – tokenised assets can be traded on digital markets more readily than traditional real estate, which typically requires significant time and cost to transact.

Greater efficiency – smart contracts automate procedures such as transfer and investor accreditation, reducing transaction complexity and cost.

Global accessibility – investors worldwide can access tokenised assets via digital platforms, removing many of the geographical frictions associated with cross-border investment.

Tokenisation Structures for Real Estate and Real Estate Debt

Tokenisation strategies for real estate and real estate debt commonly follow one of two broad structures:

Direct Ownership Tokens

The token directly represents legal ownership — or beneficial interest — in a property or specific tranche. Investors holding these tokens are effectively co-owners of the asset, receiving proportional income such as rental yield and participating in capital appreciation.

Debt-Linked Tokens

Here, tokens represent interests in a pool of debt obligations secured by real estate — mortgage-backed tokens, development finance instruments or property-backed bonds. Token holders receive contractual returns derived from interest and principal payments, comparable to traditional fixed-income securities but with the settlement and tradability benefits of blockchain infrastructure.

In both structures, a custodian or trustee typically holds the underlying legal asset on behalf of token holders, ensuring the smart-contract logic aligns with applicable legal and financial frameworks.

Applied to real estate debt, tokenisation allows mortgage pools, development or acquisition finance and property-backed bonds to be fractionalised and traded. This improves capital efficiency for originators and unlocks diversified risk exposure for investors.

Why Jersey Is an Attractive Jurisdiction

Jersey has established itself as a compelling jurisdiction for RWA tokenisation structures, particularly for real estate and related debt instruments.

Regulatory clarity

The Jersey Financial Services Commission (JFSC) has published detailed guidance specifically addressing the tokenisation of RWAs, clarifying regulatory expectations for issuers around governance, AML compliance and independent verification of underlying assets. Jersey's approach is principles-based and technology-neutral — assessing tokenised offerings on their economic reality rather than the labels applied to them. This promotes innovation while maintaining robust investor protection.

A fund-friendly environment

Jersey treats tokenisation within a well-established fund and capital markets framework. Key advantages include:

- No restrictions on the number of note holders, facilitating broad distribution

- Tax neutrality and no withholding tax, enhancing yield efficiency for international investors

- A streamlined regulatory consent process offering early confirmation of compliance before tokens are issued

These features make Jersey particularly well-suited to tokenised real estate offerings and debt products targeting institutional or professional investors and regulated markets globally.

Depth of professional infrastructure

Critically, Jersey's attractiveness is not just regulatory — it is operational. The island has a deep ecosystem of professional trustees, corporate service providers, fund and SPV administrators and digital asset specialists. SPVs can be established quickly and cost-efficiently, with service providers who understand both the traditional fund structures and the emerging tokenisation layer.

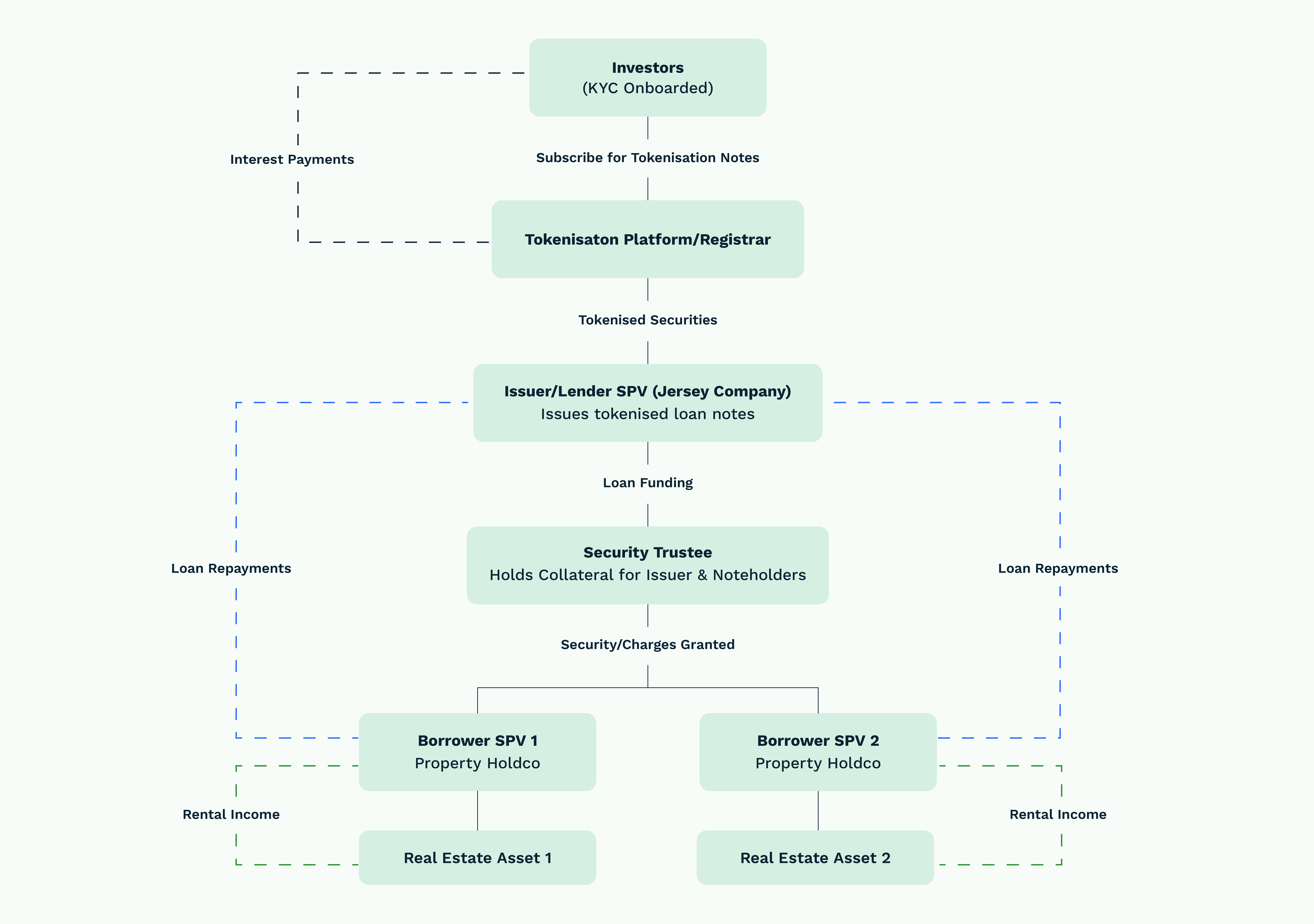

A Typical Tokenised Debt Structure

Challenges and Considerations

Tokenisation offers genuine advantages but it is not without complexity.

Liquidity depends on secondary markets and investor appetite. Tokenising an asset does not automatically create active trading. Building and maintaining liquid secondary markets requires deliberate effort and distribution strategy.

Robust custody and audit processes are also essential. Investor confidence rests on clear, professional oversight of the underlying assets and the operational framework must match the rigour of the legal and regulatory structure.

Jurisdiction and service provider selection also matter more than is often appreciated. The legal structure, the trustee, the administrator and the digital asset infrastructure all need to work in concert from day one. Retrofitting any element later is costly and disruptive. Engaging experienced professionals at the structuring stage, rather than the operational stage, is consistently the better approach.

Conclusion

Real-world asset tokenisation is moving from concept to mainstream practice, offering meaningful liquidity, accessibility and efficiency gains for real estate and real estate debt markets. As institutional and professional investor interest grows and regulatory frameworks mature, tokenisation structures are increasingly likely to become a core feature of global capital markets.

Jersey's proactive regulatory framework, fund-aligned infrastructure and deep professional services ecosystem means it is well placed to serve as a leading jurisdiction for these structures — and Whitmill's experience across fund administration, corporate services and fiduciary work positions us well to support the full lifecycle of a tokenised structure, from establishment through to ongoing operation.

To find out more about how Whitmill can support the implementation and administration of RWA tokenisation structures, get in touch with our team.